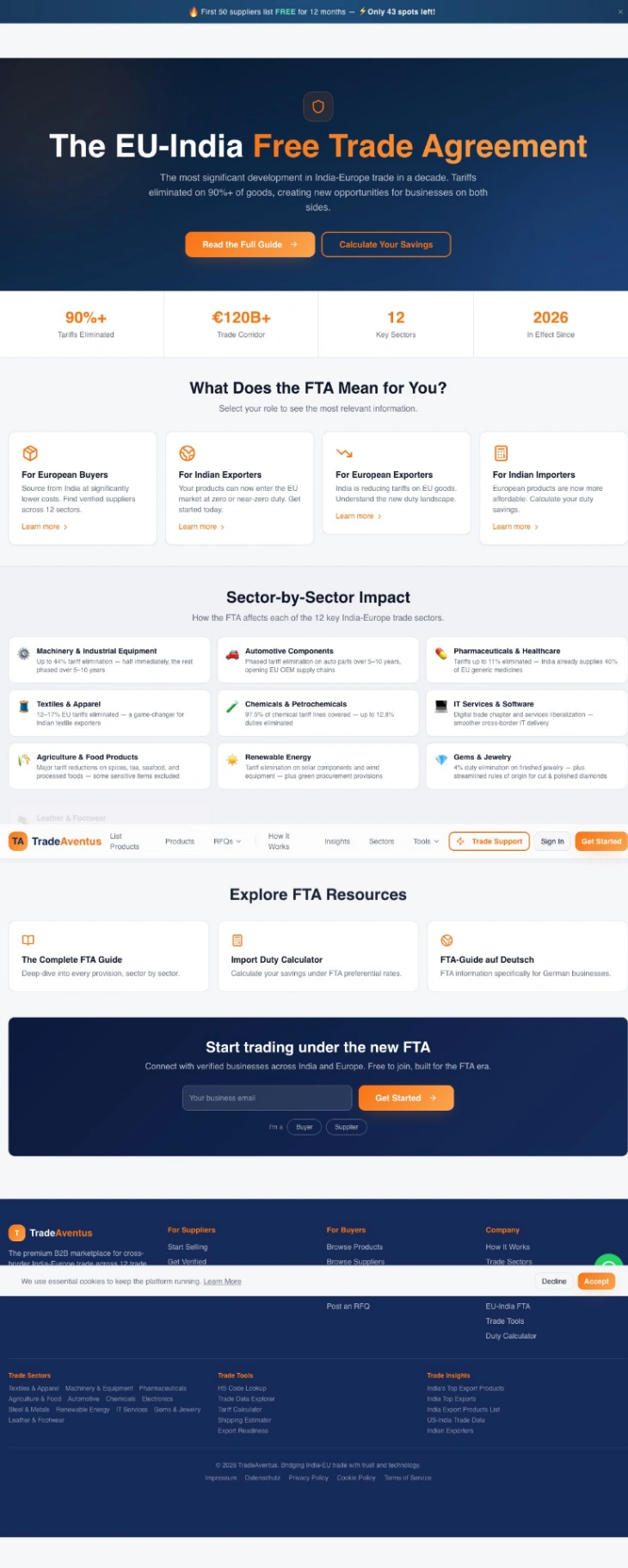

Automotive Components on TradeAventus

Automotive Components is one of the 12 strategic trade sectors connecting India and Europe on TradeAventus. Every supplier is verified before listing. Buyers contact suppliers directly — no lead fees, no middlemen, no fake leads. Quoting is ready for the incoming EU-India FTA (concluded 27 January 2026, awaiting ratification).